Incoterms (International Commercial Terms) are a set of globally recognized trade terms established by the International Chamber of Commerce (ICC) first published in 1936, updated and reissued in 2020. They define the responsibilities of buyers and sellers involved in the delivery of goods under sales contracts. Incoterms outline who is responsible for various aspects of international trade, such as shipping, insurance, import/export duties, and transportation costs. These terms are essential for avoiding misunderstandings and disputes in cross-border transactions.

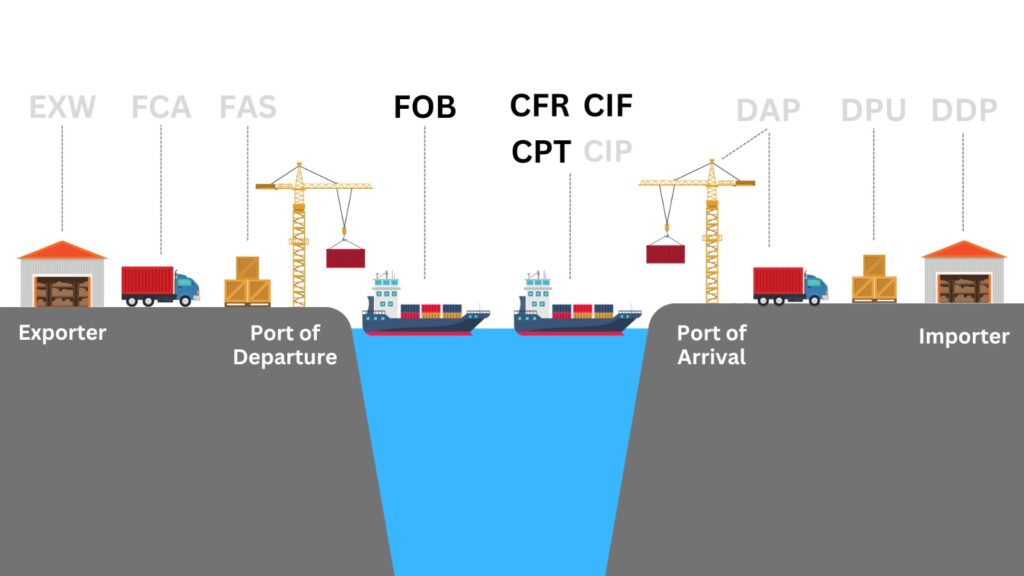

This is the third article in a 3-part series that will explain in detail what each incoterm means, what part of the trade transaction it impacts and the relative responsibilities of buyers and sellers. In this piece we will define the 4 incoterms under the Incoterms 2020 Rules For Sea and Inland Waterway Transport – FOB, CFR, CIF, and CPT.

For Incoterms EXW, FCA and FAS, please refer to Part I.

For Incoterms CIP, DAP, DPU and DDP, please refer to Part II.

Incoterms 2020 Rules For Sea And Inland Waterway Transport

8. FOB – Free on Board (named port of shipment)

Under FOB terms the seller bears all costs and risks up to the point the goods are loaded on board the vessel. The seller’s responsibility does not end at that point unless the goods are “appropriated to the contract” that is, they are “clearly set aside or otherwise identified as the contract goods”. Therefore, an FOB contract requires a seller to deliver goods on board a vessel that is to be designated by the buyer in a manner customary at the particular port. In this case, the seller must also arrange for export clearance. On the other hand, the buyer pays the cost of marine freight transportation, bill of lading fees, insurance, unloading and transportation cost from the arrival port to destination. Since Incoterms 1980 introduced the Incoterm FCA, FOB should only be used for non-containerized sea freight and inland waterway transport.

FOB is commonly used incorrectly for all modes of transport despite the contractual risks that this can introduce. In some common law countries such as the United States of America, FOB is not only connected with the carriage of goods by sea but also used for inland carriage aboard any “vessel, car or other vehicle.”

The risk of loss of or damage to the goods passes when the products are on board the vessel. The buyer bears all costs from that moment onwards.

9. CFR – Cost and Freight (named port of destination)

The seller pays for the carriage of the goods up to the named port of destination. Risk transfers to buyers when the goods have been loaded on board the ship in the country of Export. The seller is responsible for origin costs including export clearance and freight costs for carriage to the named port.

The shipper is not responsible for delivery to the final destination from the port (generally the buyer’s facilities), or for buying insurance. If the buyer requires the seller to obtain insurance, the Incoterm CIF should be considered. CFR should only be used for non-containerized sea freight and inland waterway transport; for all other modes of transport it should be replaced with CPT.

10. CIF – Cost, Insurance & Freight (named port of destination)

CIF is broadly similar to the term CFR, with the exception that the seller is required to obtain insurance for the goods while in transit. CIF requires the seller to insure the goods for 110% of the contract value under Institute Cargo Clauses (A) of the Institute of London Underwriters, or any similar set of clauses, unless specifically agreed by both parties.

The policy should be in the same currency as the contract. The seller must also turn over documents necessary, to obtain the goods from the carrier or to assert claims against an insurer to the buyer. The documents include (at a minimum) the invoice, the insurance policy, and the bill of lading. These three documents represent the cost, insurance, and freight of CIF. The seller’s obligation ends when the documents are handed over to the buyer. Then, the buyer has to pay at the agreed price. Another point to consider is that CIF should only be used for non-containerized sea freight; for all other modes of transport it should be replaced with CIP.

The seller delivers the goods on board the vessel or procures the goods already so delivered. The risk of loss of or damage to the goods passes when the goods are on the ship.

The seller must contract for and pay the costs and freight necessary to bring the goods to the named port of destination. The seller also contracts for insurance cover against the buyer’s risk of loss of or damage to the goods during the carriage.

The buyer should note that under CIF the seller is required to obtain insurance only on minimum cover. Should the buyer wish to have more insurance protection, it will need either to agree as much expressly with the seller or to make its own extra insurance arrangements.

11. CPT – Carriage Paid To (named place of destination)

The seller pays for the carriage of the goods up to the named place of destination. However, the goods are considered to be delivered when the goods have been handed over to the first or main carrier, so that the risk transfers to the buyer upon handing goods over to that carrier at the place of shipment in the country of export.

The seller is responsible for origin costs including export clearance and freight costs for carriage to the named place of destination (either the final destination such as the buyer’s facilities or a port of destination. This has to be agreed to by seller and buyer, however).

If the buyer requires the seller to obtain insurance, the Incoterm CIP should be considered instead.

iTradeDigital is simplifying international trade for businesses of all sizes, everywhere – by digitising and automating the flow of the documentation required for cross-border trade. Contact us to learn more about how we can help you simplify international trade and open up new revenue opportunities for your business or simply register online to get started.

– ##### –

Authors:

John Dunlop is a trade finance expert with over thirty years of experience in managing letter of credit and collection transactions from purchase order to final payment. Previously CEO of InterNetLC.com and is currently a Team Leader at iTradeDigital IOM Ltd.

Tony Kavanagh is a technology executive with over 25 years of experience in building brands and driving demand for companies of all sizes, globally. Skilled in GTM strategy, product marketing, PR/AR and CRM success, Tony has held senior positions at KPMG, Oracle, Salesforce, DataStax, Insightly, & XOJET. He is currently CMO at iTradeDigital IOM Ltd.

– ##### –